Overview of 401(k) Withdrawal Penalties

401(k) withdrawal penalties are fees imposed by the IRS on early withdrawals from a 401(k) retirement account before the age of 59 1/2. The purpose of these penalties is to discourage individuals from dipping into their retirement savings prematurely and ensure that the funds are used for their intended purpose – retirement.

Common scenarios where these penalties may apply include:

Early Withdrawals

- Withdrawing funds before the age of 59 1/2 for non-qualifying reasons.

- Using the funds for purposes other than retirement, such as buying a home or paying off debt.

Early Withdrawal Penalties

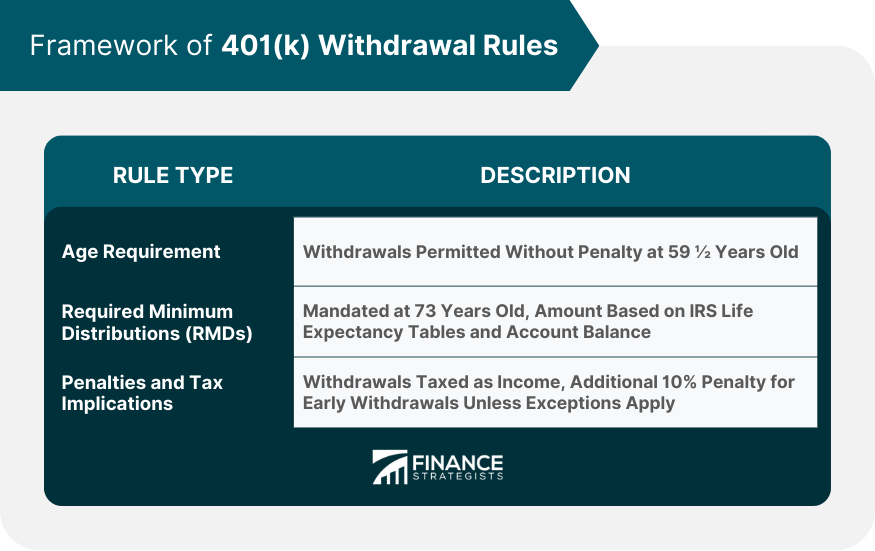

Withdrawing funds from a 401(k) before the age of 59 1/2 can result in significant penalties that impact your retirement savings.

Penalties for Early Withdrawal

Early withdrawal from a 401(k) typically incurs a penalty of 10% on the amount withdrawn in addition to any applicable taxes.

Impact on Retirement Savings

- Reduced retirement nest egg: Early withdrawals can significantly diminish the amount of funds available for retirement, potentially jeopardizing your financial security in later years.

- Lost compound interest: By taking out funds early, you miss out on the opportunity for your investments to grow through compound interest over time.

Additional Taxes

Aside from the penalty for early withdrawal, the amount taken out is also subject to income tax. This means that not only do you lose a portion of your funds immediately, but you also have to pay taxes on the withdrawn amount, further reducing your overall retirement savings.

Exceptions to Penalties

When it comes to 401(k) withdrawal penalties, there are certain circumstances where individuals may be able to avoid or minimize these penalties. These exceptions are important to understand to make informed decisions about your retirement savings.

Hardship Withdrawals

One common exception to 401(k) withdrawal penalties is in cases of hardship withdrawals. This typically applies when an individual faces immediate and heavy financial need, such as medical expenses, funeral costs, or preventing foreclosure on a primary residence. In such situations, penalties may be waived, but taxes may still apply.

Age Exceptions

Another exception to early withdrawal penalties is based on age. If you are at least 59 ½ years old, you are generally exempt from early withdrawal penalties. This is because you have reached the age when you can start withdrawing from your 401(k) without facing additional penalties.

Employment Status

In certain cases, if you separate from your employer at age 55 or later, you may be able to take penalty-free withdrawals from your 401(k). This exception applies to 401(k) plans sponsored by your current employer, not previous employers.

Impact on Retirement Savings

Withdrawing funds from your 401(k) before reaching retirement age can have a significant impact on your long-term retirement savings. Let’s explore how penalties affect the growth of your retirement funds and compare the financial implications of early withdrawals versus waiting until retirement age.

Effect of Penalties on Long-Term Growth

Early withdrawals from your 401(k) can have a detrimental effect on the long-term growth of your retirement savings. Not only do you lose the principal amount withdrawn, but you also miss out on potential investment gains over time. The compounding effect of these lost earnings can significantly reduce the overall value of your retirement account.

Comparing Early Withdrawals vs. Waiting Until Retirement Age

When you withdraw funds from your 401(k) early, you not only incur penalties but also miss out on the opportunity for your investments to grow tax-deferred over time. On the other hand, waiting until retirement age allows your investments to continue growing without penalties, maximizing the potential value of your retirement savings.

Strategies to Mitigate Impact of Penalties

- Consider alternative sources of funding before tapping into your 401(k) early, such as emergency savings or low-interest loans.

- If faced with a financial hardship, explore hardship withdrawal options or loans available through your 401(k) plan, which may have lower penalties or repayment terms.

- Consult with a financial advisor to explore other retirement savings options or strategies to minimize the impact of penalties on your overall retirement plan.